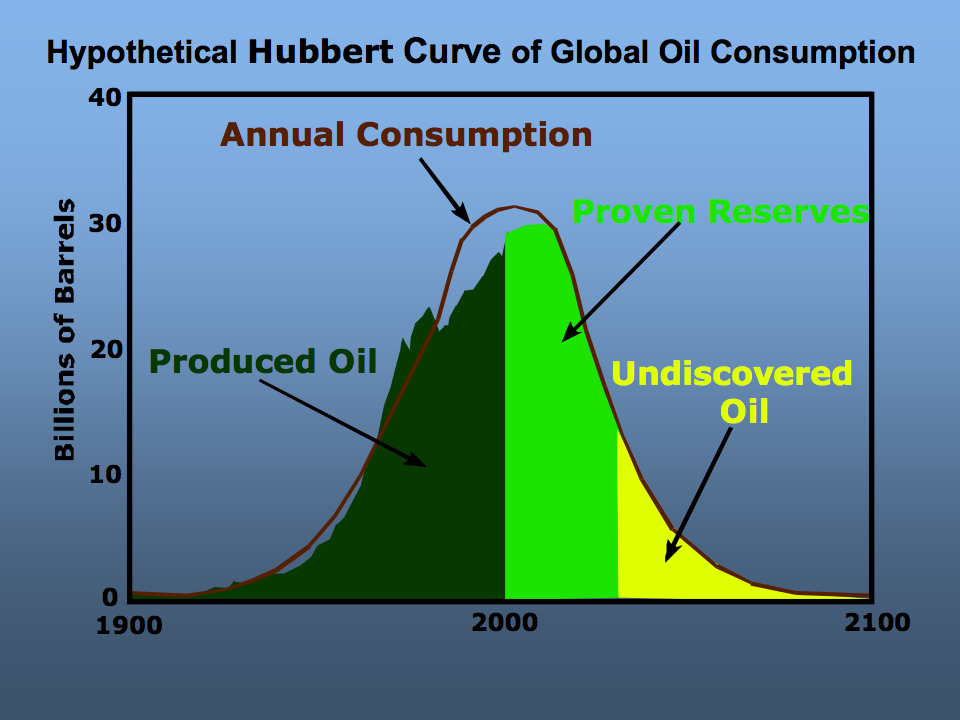

The Hubbert peak oil forecast assumes the production of oil (or gas or other commodities) follows a logistics curve from initial production to final resource exhaustion. The area under the “Hubbert Peak Oil” curve represents the total oil to be produced, or the total oil resource that has and will be exploited. The curve represents the volume of oil produced per unit time. In most forecasts, years or decades represent the unit time. We can read the curve as barrels of oil produced per year or per decade.

Economists consider supply and demand to be functions of price. The volume of a product consumed in day or a year or other time period is thus considered to be a function of the average price for that time period. If we want to perform a forecast of peak oil or ultimate oil consumption for a oil producing province, or a country, or the world, then we would like to have a forecast of the oil price for the remaining history of oil production. This is a difficult problem. Consider an example from 1983:

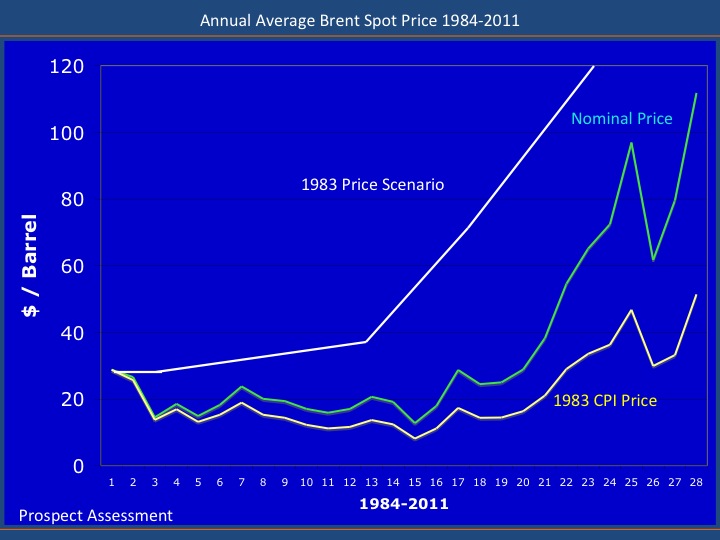

The figure shows a price forecast made by a major oil company. It was used to evaluate potential projects in a variety of basin and countries. It was also used to forecast company revenues from existing production. Discussions with colleagues working in other companies and host governments at the time suggested that this scenario was similar to scenarios used throughout the industry.

At the time of the forecast, Brent crude traded for about $30 a barrel. Although the price was forecast to remain flat for a few years, by 1986 it was expect to begin rising modestly each year until about 1997. From then until the end of the forecast period, it was forecast to rise to $120 a barrel.

The figure shows the actual price oil in nominal terms through 2011. The nominal price of oil fell to below $20 a barrel for 16 years, with only a few brief intervals above $20. It reached its nadir in December, 1998 at less than $10 a barrel. (http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=RBRTE&f=M)

From then it rose, with one pause, to over $100. Although it never averaged $120 per barrel for an entire year, it did average over $120 a barrel in April 2011 and March 2012.

Nominal prices do not reflect inflation. For much of the forecast period inflation fell, becoming quite low in recent years. Using the CPI to discount the nominal price to 1983 dollars shows the price never came close to $100 a barrel, and has only recently approached $50 a barrel in 1983 dollars.

From today’s perspective, the error in the 1983 forecast may seem obvious. Oil production was increasing in North America and the North Sea at that time. OPEC members were cheating on their quotas. The high oil prices of the previous decade led to increased transportation fuel efficiency, as well as fuel substitution in many sectors of the economy.

In 1970, however, it seemed that oil would remain below $5 a barrel for many years. The Arab oil boycott just a few years later was not foreseen. For many years a nominal price above $3 a barrel seemed far fetched.

Not knowing the future price of oil, it is very problematic to assume the future production of oil will follow a simple logistic curve. This should give pause to those who predict either a near term collapse in production or a future with abundant supplies.