OPEC concluded the November meeting last week by agreeing to leave their production quota unchanged. A press release was issued after the meeting: http://www.opec.org/opec_web/en/press_room/2938.htm

The most important paragraphs read:

The Conference reviewed the oil market outlook, as presented by the Secretary General, in particular supply/demand projections for the first, second, third and fourth quarters of 2015, with emphasis on the first half of the year. The Conference also considered forecasts for the world economic outlook and noted that the global economic recovery was continuing, albeit very slowly and unevenly spread, with growth forecast at 3.2% for 2014 and 3.6% for 2015.

The Conference also noted, importantly, that, although world oil demand is forecast to increase during the year 2015, this will, yet again, be offset by the projected increase of 1.36 mb/d in non-OPEC supply. The increase in oil and product stock levels in OECD countries, where days of forward cover are comfortably above the five-year average, coupled with the on-going rise in non-OECD inventories, are indications of an extremely well-supplied market.

Recording its concern over the rapid decline in oil prices in recent months, the Conference concurred that stable oil prices – at a level which did not affect global economic growth but which, at the same time, allowed producers to receive a decent income and to invest to meet future demand – were vital for world economic wellbeing. Accordingly, in the interest of restoring market equilibrium, the Conference decided to maintain the production level of 30.0 mb/d, as was agreed in December 2011.

The New York Times, Financial Times, and other news sources report some disagreement among OPEC’s members about this decision. Some countries, such as Algeria, Iraq, Venezuela, and Nigeria, would prefer to reduce production in order to raise the spot price. Presumable the reduction would be made by Saudi Arabia.

The Saudis are unwilling to do this, which has produced some speculation about their motives at this time. One line of thought is that the Saudis are in league with the US government: by driving down the price of oil, the Russian Ruble declines and Russian foreign income declines. The other line of thought is that the Saudis wish to preserve their sales to the US.

I prefer the latter scenario, which echoes the dispute between Venezuela and Saudi Arabia from 1998 to 2001. At that time oil production increased in Venezuela due to a field reactivation program executed by PEDEVSA, the state oil company. The program was first announced in 1989 and required several years to come into effect. Under this program, international oil companies (EXXON, BP, and so on) entered into contracts to improve production from existing fields and to explore for new fields within defined concession areas. The resulting increased oil production entered the US market, displacing Saudi exports to the US.

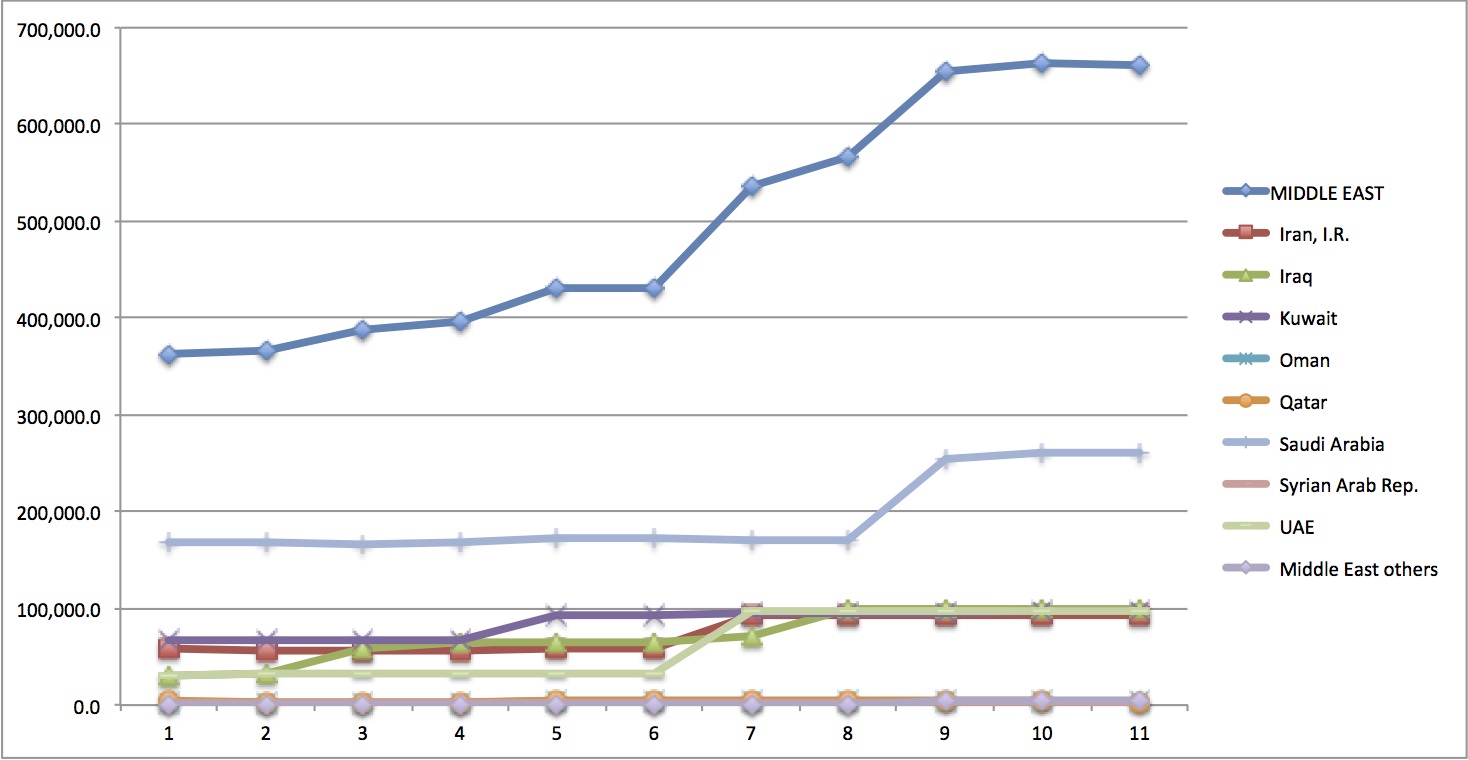

The chart above shows Saudi oil imports to the US from 1990 to 2014. Common wisdom in some quarters is that the Saudis want to export one million barrels per day to the US as a matter of foreign policy. The decline at the beginning of the period represents the displacement of Saudi imports by Venezuelan imports. The steep increase between 1999 and 2002 represents the increase in Saudi production intended to reduce the price of oil and remove more expensive Venezuelan crude from the US market. The steep fall at the end of the chart represents the displacement of Saudi crude by US shale oil production, primarily from the Bakken Formation in North Dakota.

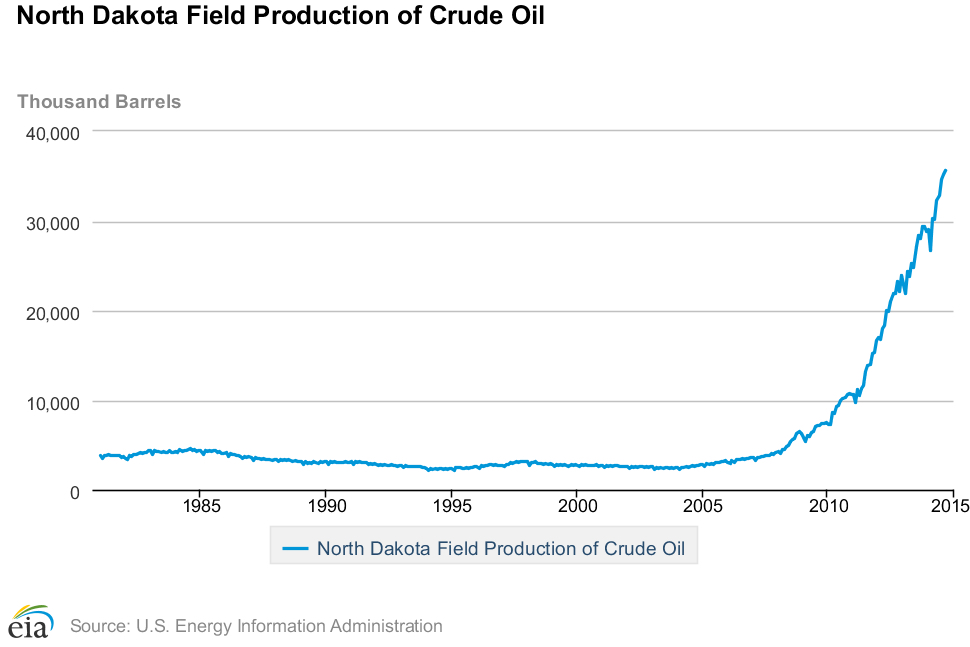

This chart shows oil production from North Dakota between 1990 and 2014. The steep increase in production beginning in 2008 represents new shale oil production from the Bakken Formation.

Why did the Saudis wait six years to respond to the increase in Bakken production? Between 2008 and 2012 Bakken production replaced declining oil production within the US, primarily from the Alaska North Slope fields. During the past two years, increasing Bakken and Eagle Ford oil shale production has exceeded field declines elsewhere in the US. Some foreign oil was displaced by the increase in US production, and some of the oil was imported from Saudi Arabia.

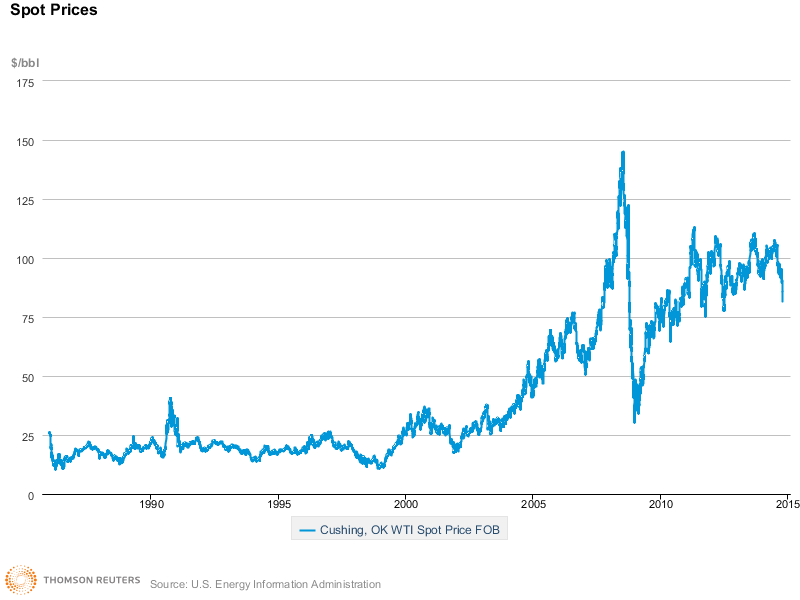

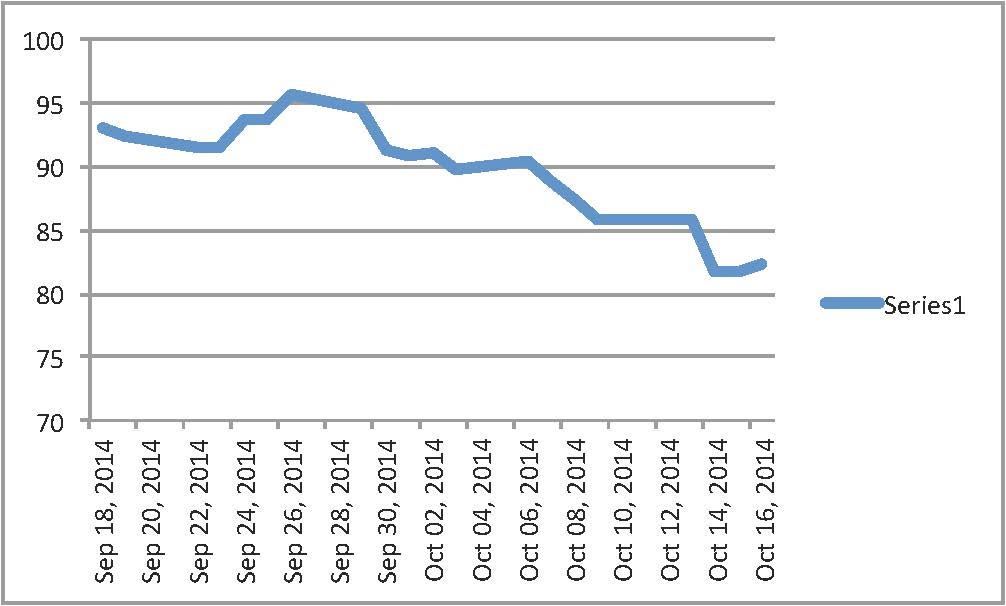

Today West Texas Intermediate crude oil closed down 94 cents at $65.84/barrel. The price of oil has been declining for several months, as noted in earlier posts. How much lower can it go before oil shale wells are shut in?

Only the well operators know the answer to this question, and it varies for each well. These shale oil wells begin production at a high daily rate, but after a three to nine months the production rate declines rapidly. Once the price oil sinks below the cost of shale oil production, we can expect a fairly rapid fall in production over the course of year or so. During this time, oil imports will likely rise.

There is a leading indicator for those looking at the shale oil play from the outside: the rig count. When operators decide there is no financial incentive to drill new production wells, they stop contracting drilling rigs. Baker Hughes publishes a survey of rigs every week:

http://phx.corporate-ir.net/phoenix.zhtml?c=79687&p=irol-rigcountsoverview

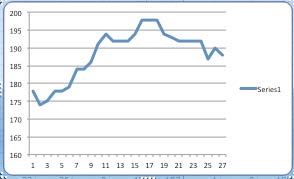

For reference, below is a chart of recent North Dakota rig counts:

The above chart shows the number of rigs operating in North Dakota from June 6 to December 4, 2014. Good weather during the spring and summer typically results in an increase in rig use. Winter weather typically impedes the movement of both rigs and supplies to new drill sites, so the rig count declines.

For context, here is a longer term view of North Dakota rig counts:

This chart shows the rig count in North Dakota from March, 2011 to December, 2014. The peak in rig count reflects the entry of new players as operators realized there was a resource to exploit in 2012-2013. The interesting question over the coming months is this: if the price of oil falls, will these operators stop drilling wells? Will the rig count fall dramatically?