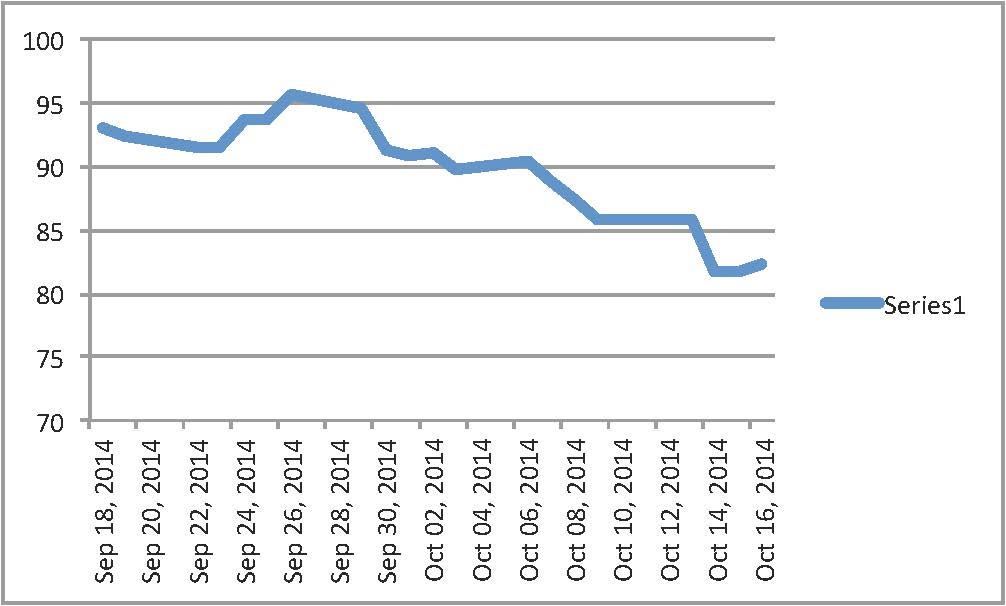

The price of crude oil has recently fallen from over $100/barrel to below $85/barrel.

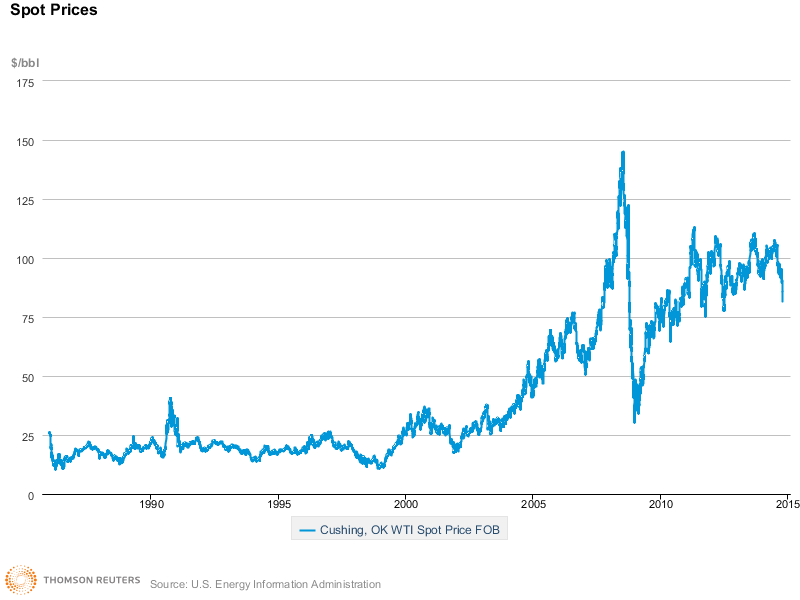

As the chart shows, for many decades the price of oil was below $50/barrel until the turn of the century, when the price rose over the course of ten years to a peak above $115/barrel. The price fell dramatically during the 2008-2009 recession. Until a few weeks ago it increased from below $40/barrel to a recent average close to $100/barrel. The one hundred dollar barrel appeared to be the “new normal”, which encouraged US companies to pursue shale oil in North Dakota and more recently in the Texas. A few weeks ago the price started to fall:

This chart show the price of West Texas Intermediate (WTI) crude at the Cushing, Oklahoma terminal. Is this a trend that will continue? Why has it occurred? Who will benefit? These questions have been addressed by news articles and op ed pieces in a variety of outlets. National Public Radio aired a report on Saudi Arabia’s possible role in the fall of prices

http://www.npr.org/2014/10/16/356588376/crude-oil-prices-drop-as-saudis-refuse-to-cut-production

Thomas Friedman’s column in the NY Times suggests the Saudi’s are driving the price down through high production in order to reduce US shale oil production and to damage Iran’s ability to support Shia militants:

He also suggests that perhaps the US and the Saudi’s want to damage Russia’s economy by reducing its revenues from oil exports.

The Financial Times, the Wall Street Journal, and many other papers have run similar stories. Many stories claim that the decline in economic activity in Europe and China during the past six months hasreduced demand for oil, and thus caused the price to fall since the beginning of the year. Is this true?

Regarding China’s oil consumption, Platt’s reports that China has imported 7.4 percent more oil for the 12 months ending September 30 than it did a year earlier. China’s average import was 6.74 million barrels of oil per day. This was 13 percent higher than in August, 2014.

Regarding Europe, the International Energy Agency (IEA) reported in September that first quarter 2014 consumption was 13.7 million barrels per day (mmbpd), second quarter consumption was 14.1 mmbpd, and third quarter was estimated to be 14.6 mmbpd.

Falling demand in China and Europe is not depressing prices.

The IEA also reports falling supplies in August. These are due in part to seasonal maintenance in several producing countries, and a smaller call for deliveries of crude from Saudi Arabia.

http://www.iea.org/oilmarketreport/omrpublic/currentreport/#Supply

Economic data is always retrospective. Reports of production and consumption arrive well after the crude has been pumped from wells or delivered to refineries. In a few months we will have a better idea how much oil is being supplied and consumed this autumn.

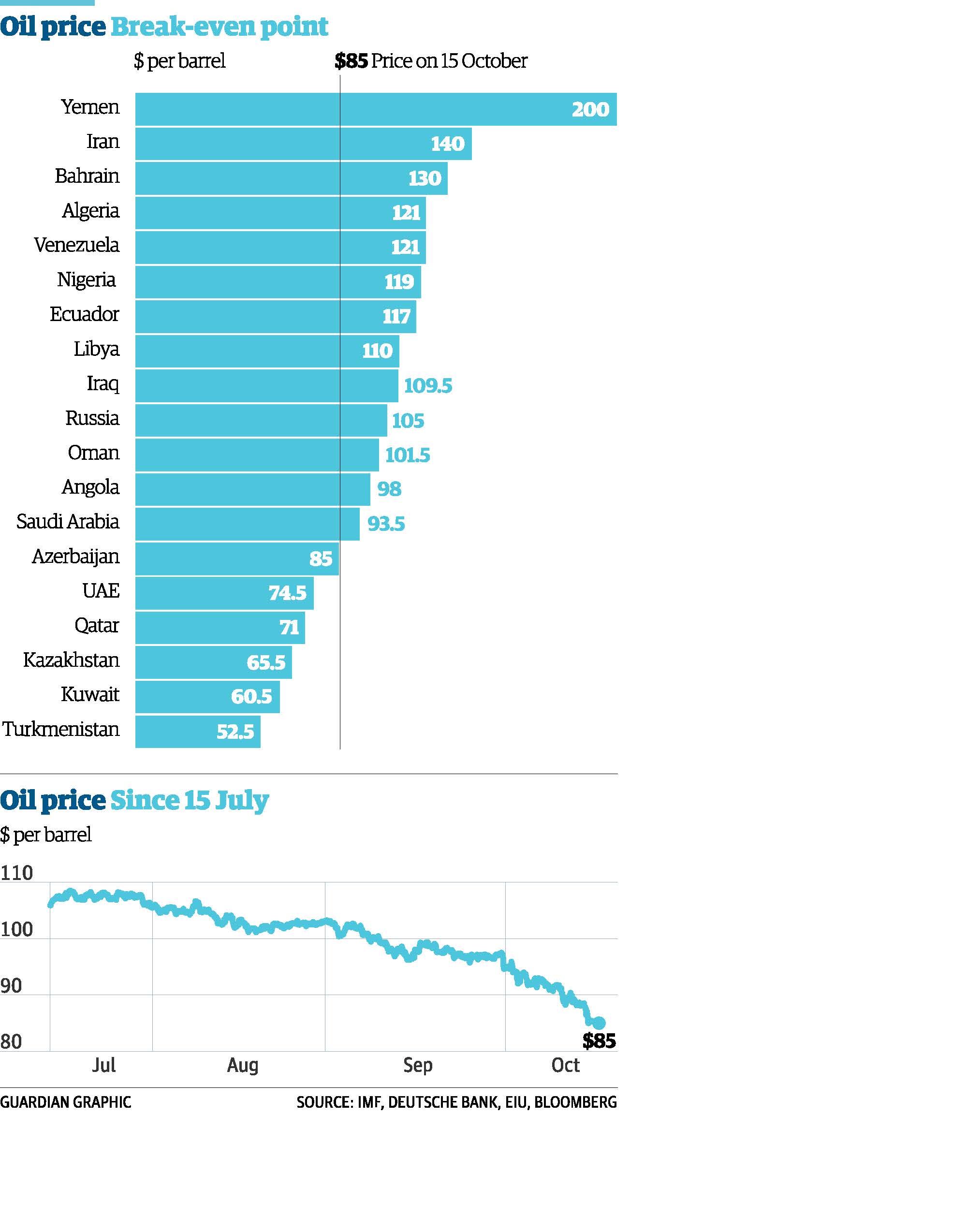

What happens if crude oil prices remain low? This topic also generates opinion pieces. The Guardian had piece with one interesting graphic:

The bar graph at the top of figure shows the price of oil needed for producers to break even in 19 exporting countries. Published on October 15 when the price for WTI was near $85/barrel, it shows that Iran loses perhaps $50/barrel. Iran produces oil from a number of fields, and no doubt some fields break even below $85/barrel. But the chart indicates that some, perhaps most, of Iran’s fields will lose money if recent prices persist. Likewise, Russia loses about $20/barrel at recent prices. However, Russia produces oil from many fields. No doubt some fields lose money at recent price levels, but others will remain profitable. Low prices will damage Russia’s foreign income.

As for Saudi Arabia, if it does play an active, deliberate role in driving prices down, it has some fields that lose money, but most will make money. With substantial foreign reserve holdings, it may be able to live with low prices for a longer period of time than other members of OPEC.

As for US oil shale, the cost of lifting a barrel of crude vary within basins from $60 a barrel to $80 a barrel. If low prices persist, then investors in US shale projects will find less comfort with these project than when the price was a the “new normal” of $100 a barrel. As the perception of risk in shale oil projects rises, some investors will look for projects in other fields.

OPEC energy ministers will meet in Vienna on November 27. Statements made before and after meeting may provide some guidance about future production trends. These statements may hint at political conflicts between member states, and between OPEC members and other producing countries.